Running a small or medium-sized business means making dozens of financial decisions every single week, pricing a new product, hiring an extra employee, investing in equipment, or expanding to a second location. Most business owners make these calls based on gut instinct or rough estimates. But there is a straightforward financial tool that can bring hard numbers to every one of those decisions: break-even analysis.

Break-even analysis answers one of the most fundamental questions in business: How much do I need to sell just to cover my costs? Once you know your break-even point, you can price with confidence, plan with clarity, and grow without guessing.

We will help you through everything you need to know about break-even analysis, what it is, how to calculate it, and how to put it to practical use in your business. In case you are a bakery owner, an IT consultant, a retail shop, or a manufacturing firm, this tool works across all industries.

What Is Break-Even Analysis?

Break-even analysis is a financial calculation that tells you the exact point at which your total revenues equal your total costs, meaning you are neither making a profit nor suffering a loss. That point is called the break-even point (BEP).

Think of it this way: every business has costs that need to be paid regardless of how much it sells (like rent or salaries), and costs that go up as it sells more (like raw materials or packaging). Break-even analysis maps out when your sales revenue is finally large enough to cover all of those costs combined.

Beyond the break-even point, every additional unit you sell generates pure profit. Below it, you are operating at a loss. Knowing where that line sits is essential for any business owner who wants to stay in control of their finances.

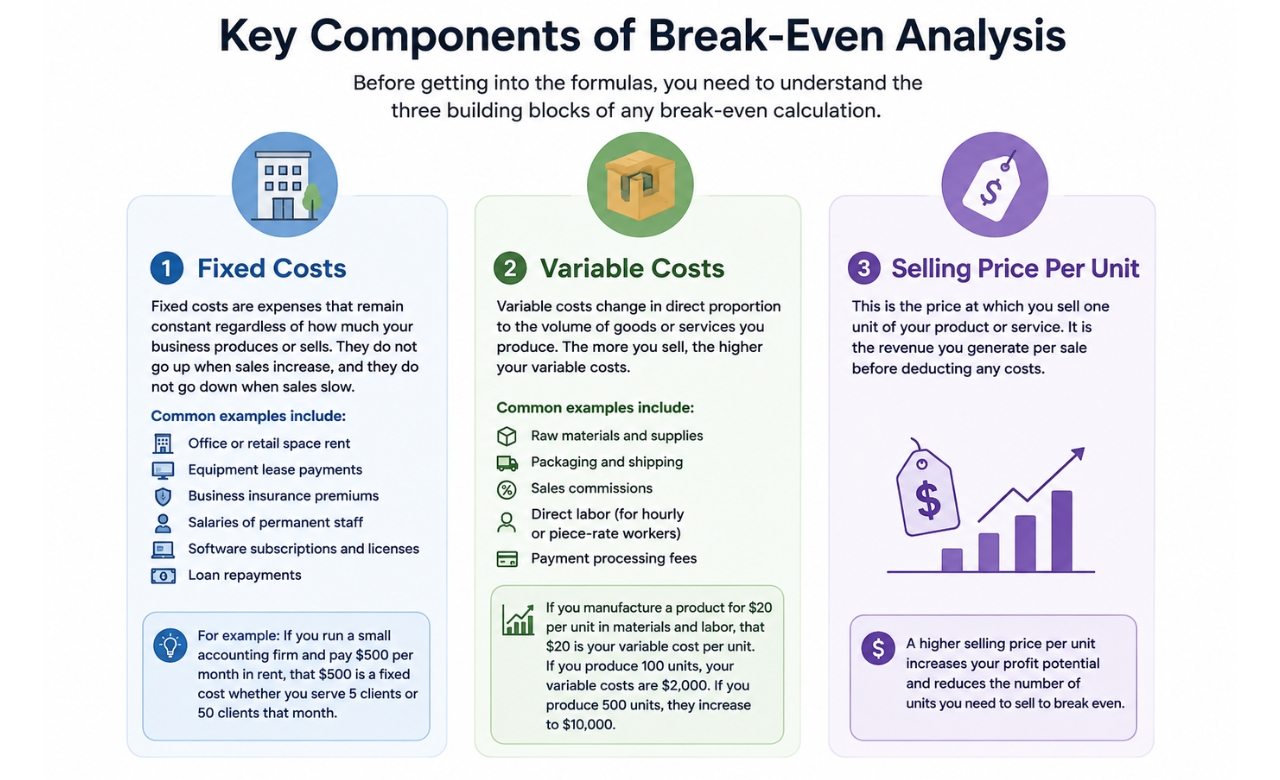

Key Components of Break-Even Analysis

Before getting into the formulas, you need to understand the three building blocks of any break-even calculation.

1. Fixed Costs

Fixed costs are expenses that remain constant regardless of how much your business produces or sells. They do not go up when sales increase, and they do not go down when sales slow.

Common examples of fixed costs include:

- Office or retail space rent

- Equipment lease payments

- Business insurance premiums

- Salaries of permanent staff

- Software subscriptions and licenses

- Loan repayments

For example, if you run a small accounting firm and pay $500 per month in rent, that $500 is a fixed cost whether you serve 5 clients or 50 clients that month.

2. Variable Costs

Variable costs change in direct proportion to the volume of goods or services you produce. The more you sell, the higher your variable costs.

Common examples of variable costs include:

- Raw materials and supplies

- Packaging and shipping

- Sales commissions

- Direct labor (for hourly or piece-rate workers)

- Payment processing fees

If you manufacture a product for $20 per unit in materials and labor, that $20 is your variable cost per unit. If you produce 100 units, your variable costs are $2,000. If you produce 500 units, they increase to $10,000.

3. Selling Price Per Unit

This is the price at which you sell one unit of your product or service. It is the revenue you generate per sale before deducting any costs.

The Break-Even Analysis Formula

Now that you understand the three components, here are the core formulas you need.

Contribution Margin Per Unit

Before calculating the break-even point, you need your contribution margin, the amount each sale contributes toward covering fixed costs (and eventually, generating profit).

Contribution Margin = Selling Price Per Unit − Variable Cost Per Unit

Break-Even Point in Units

Break-Even Point (Units) = Fixed Costs ÷ Contribution Margin Per Unit

Break-Even Point in Revenue (Sales Dollars)

Break-Even Point (Revenue) = Fixed Costs ÷ Contribution Margin Ratio

Contribution Margin Ratio = Contribution Margin Per Unit ÷ Selling Price Per Unit

- Check out our Break-Even Point Calculator

Break-Even Analysis: A Step-by-Step Example

Let us walk through a realistic example for a small business.

Scenario:

Emily runs a small candle-making business. Here are her numbers:

- Monthly fixed costs: $3,000 (rent, insurance, equipment)

- Variable cost per candle: $8 (wax, wick, jar, packaging)

- Selling price per candle: $20

Step 1 — Calculate the Contribution Margin:

$20 − $8 = $12 per candle

Every candle Emily sells contributes $12 toward covering her fixed costs.

Step 2 — Calculate the Break-Even Point in Units:

$3,000 ÷ $12 = 250 candles per month

Emily needs to sell 250 candles every month just to break even. Below that, she is operating at a loss. Every candle sold beyond 250 earns her $12 in profit.

Step 3 — Calculate the Break-Even Point in Revenue:

Contribution Margin Ratio = $12 ÷ $20 = 0.60 (or 60%)

Break-Even Revenue = $3,000 ÷ 0.60 = $5,000 per month

Emily needs $5,000 in monthly sales to cover all her costs.

How to Use Break-Even Analysis in Your Business

Calculating your break-even point is just the beginning. Here is how to actually put it to work for smarter decision-making.

1. Setting and Validating Your Prices

One of the most common mistakes small business owners make is pricing based on what competitors charge or what “feels right.” Break-even analysis forces you to price based on your actual costs.

Run your break-even calculation at different price points and ask yourself: at this price, how many units do I realistically need to sell? If the answer seems achievable given your market, the price works.

If you need to sell 5,000 units per month in a market that can only support 500, you need to revisit your pricing or cost structure.

2. Evaluating New Products or Services

Before launching anything new, run a break-even analysis for it. Estimate the fixed costs you will incur (equipment, marketing, setup), the variable costs per unit, and a realistic selling price.

Your break-even analysis will tell you the minimum sales volume needed. If that volume seems unrealistic, you have saved yourself from a costly mistake before spending a single dollar.

3. Planning for Growth and Investment

Thinking about hiring a new employee, opening a second branch, or buying a new piece of equipment? Each of these decisions increases your fixed costs.

By plugging the new fixed cost figure into your break-even formula, you can immediately see how much more you need to sell each month to justify that investment. This turns vague business intuition into a clear, measurable target.

4. Securing Loans and Attracting Investors

Lenders and investors want to see that you understand your numbers. Walking into a bank meeting with a clear break-even analysis demonstrates financial literacy and gives your projections credibility.

It shows exactly when your business will become profitable, which dramatically increases confidence in your ability to repay a loan or deliver returns.

5. Managing Cash Flow During Slow Seasons

Many small and medium businesses experience seasonal fluctuations. Break-even analysis helps you prepare. During your high season, knowing your break-even point tells you how much surplus you are generating, surplus that can be set aside to cover the slow months.

During slow months, you know exactly how far below break-even you are and can make informed decisions about cutting variable costs or running promotions to close the gap.

Break-Even Analysis for Service Businesses

Most break-even examples use product-based businesses, but the concept applies equally well, and is just as powerful, for service businesses such as accounting firms, consulting practices, freelancers, salons, and repair shops.

For a service business, think of your “unit” as a billable hour, a client, or a project.

Example:

Michael runs a small IT consulting firm.

- Monthly fixed costs: $12,000 (office, staff salaries, software)

- Variable cost per consulting hour: $40 (subcontractor fees, transport)

- Billing rate per hour: $120

Contribution Margin:

$120 − $40 = $80 per hour

Break-Even Hours:

$12,000 ÷ $80 = 150 billable hours per month

Michael now knows that he must bill at least 150 hours per month to cover all his costs. He can plan his client load, schedule, and marketing efforts more effectively with this number.

Common Mistakes to Avoid in Break-Even Analysis

Even a simple tool can be misused. Watch out for these frequent errors

1. Incorrectly Categorizing Expenses

A major mistake in break-even analysis is placing expenses in the wrong category. Some business costs stay constant, while others increase as sales grow. Certain expenses, such as utility bills, may contain both fixed and variable portions.

Separating these costs correctly is important because inaccurate classifications can completely change your break-even calculation. If needed, seek help from an accountant or financial professional to organize your costs properly.

2. Working With Old Financial Data

Your break-even point should always be based on current numbers. Changes in rent, supplier pricing, wages, subscriptions, or operational expenses can directly affect your calculations.

Using outdated figures may give you a false sense of profitability and lead to poor planning decisions. Regularly reviewing your financial data keeps your analysis realistic and dependable.

3. Leaving Out Taxes and Asset Costs

Some businesses calculate break-even without considering taxes, depreciation, or long-term equipment expenses. This often creates an overly optimistic financial picture.

Including these additional costs gives you a more accurate understanding of how much revenue your business truly needs to remain financially stable.

4. Thinking Break-Even Means Success

Breaking even only means your income matches your expenses. It does not mean your business is earning profit.

Your break-even point should be treated as the minimum requirement to stay operational. The real goal is to generate consistent profits that allow your business to grow, expand, and handle unexpected challenges.

5. Excluding the Owner’s Salary

Many freelancers and small business owners forget to include their personal salary in business expenses. As a result, the business may appear profitable even though the owner is not earning a sustainable income.

Adding owner compensation to fixed costs provides a more realistic view of the business’s actual financial health.

Break-Even Analysis vs. Profit Goal Analysis

Once you understand break-even analysis, you can easily extend it to set profit targets.

Target Profit Formula:

Units Needed = (Fixed Costs + Target Profit) ÷ Contribution Margin Per Unit

Going back to Emily’s candle business, if she wants to earn an additional profit of $2,400 per month after covering her fixed costs, the calculation becomes:

($30,00 + $24,000) ÷ Rs. 12 = 450 candles per month

Emily now knows she needs to sell 450 candles per month to cover her expenses and achieve her desired monthly profit goal.

This gives her a clear and measurable sales target instead of relying on a vague objective like “increase sales.”

Using Break-Even Analysis With Multiple Products

If your business sells more than one product or service, the analysis becomes slightly more complex. You will need to calculate a weighted average contribution margin based on your expected sales mix.

For example, if your business sells two products, Product A and Product B, and you expect to sell them in a 60:40 ratio, you would weight each product’s contribution margin by its share of total sales and average them together. This gives you a blended contribution margin to use in your break-even formula.

A professional bookkeeper or accountant can help you set up a multi-product break-even model tailored to your specific business, ensuring that your product mix assumptions are realistic and your analysis is accurate.

How Professional Bookkeeping Improves Break-Even Accuracy

Break-even analysis is only as reliable as the financial data behind it. Inaccurate bookkeeping leads to inaccurate break-even numbers, which leads to poor decisions. This is where professional bookkeeping and accounting services make a direct impact on your bottom line.

A professional bookkeeper will:

- Accurately categorize every expense as fixed or variable

- Maintain up-to-date records so your numbers always reflect the current reality

- Prepare profit and loss statements that make it easy to identify your true cost structure

- Help you track your contribution margins by product or service line

- Work with your accountant to ensure tax liabilities are factored into your analysis

When your books are clean and current, running a break-even analysis takes minutes, and the results you get are numbers you can actually trust.

- Learn More about our Small Business Bookkeeping & Accounting in the USA

Frequently Asked Questions About Break-Even Analysis

How often should I recalculate my break-even point?

At a minimum, recalculate whenever there is a significant change in your cost structure or pricing, a rent increase, a supplier price change, a new hire, or a price revision. Many businesses benefit from running a fresh break-even analysis quarterly as part of their financial review.

Can break-even analysis predict when my business will become profitable?

Not on its own. Break-even tells you the volume required for profitability, but to project when you will reach that volume, you need to combine it with a sales forecast. Your accountant can help you build a simple financial model that integrates both.

Is break-even analysis useful for an established business, or just for startups?

Both. Startups use it to validate business models. Established businesses use it to evaluate new initiatives, justify price changes, and manage profitability during difficult periods.

What if my variable costs are difficult to pin down?

This is common for service businesses with fluctuating costs. A professional bookkeeper can help you analyze historical data to arrive at a reliable average variable cost figure.

Turn Your Numbers Into Decisions

Break-even analysis is not complicated — but it is powerful. For small and medium businesses operating in competitive, resource-constrained environments, it is one of the most practical financial tools available.

It gives you a clear, objective answer to the most important question in business: Are the numbers in my favor?

By understanding your fixed costs, variable costs, and contribution margins, you can price strategically, invest wisely, plan for growth, and sleep a little easier at night knowing exactly where your business stands.

If you are not sure where to start, or if your books need cleaning up before a reliable break-even analysis is possible, our bookkeeping and accounting team is here to help. We work with small and medium businesses to get their numbers right, so they can make better decisions, faster.

Ready to take control of your business finances? Contact us today for a free consultation.

This article was written by our accounting and bookkeeping team. We specialize in helping small and medium businesses understand their numbers and make confident financial decisions.